Think of sending money to your friend and not incurring even a single fee, with the transaction completed in just a few minutes. This is what millions of Americans experience with Zelle on a daily basis. In today’s busy and fast-moving digital economy, it’s important to understand how does Zelle make money, especially in 2024—a year in which the platform processed an estimated over one trillion dollars in transactions without charging users a single cent. This apparent paradox raises compelling questions about modern fintech business models and how large-scale payment networks generate value without relying on direct consumer fees.

Compared to the traditional payment services that charge nickel and dime to users in terms of transaction charges, Zelle uses a completely different revenue model. Zelle is one of the most prominent peer-to-peer networked payment systems in America with more than 151 million registered accounts and has redefined the way money flows in and out of bank accounts. This is a detailed reference on the innovative processes that make up the business model of Zelle and how Zelle actually generates revenues and sustains the use of the service by ordinary people.

What Is Zelle?

Zelle is a peer-to-peer money transfer system that allows immediate transfers of money between bank accounts in the United States. Zelle was introduced in 2017 by Early Warning Services LLC and enables users to send and receive money with nothing more than an email address or a mobile phone number, and the transaction is usually completed within minutes. As the platform continues to scale, many users and analysts ask how does Zelle make money despite offering these services at no direct cost to consumers.

The platform functions in a different way in comparison to the competitors as it is directly embedded in mobile banking apps and online portals of more than 2,200 financial institutions. The peculiarity of Zelle is that this system of money transfer is bank-to-bank, i. e. the money is transferred between two accounts without being stored on a separate digital wallet, which increases its security and convenience of users.

Popularity

The fact that Zelle has since its launch exploded proves its leadership in the digital payment market:

- High levels of transaction volume: Zelle has the largest volume of interim transaction in 2024 carrying over 1 trillion dollars.

- User Base Growth: the platform had 151 million registered consumer and small business accounts by 2024, and is expected to have 73.2 million active users.

- Number of transactions: In 2022, the number of transactions completed by users was more than 2.3 billion, and the figure is steadily increasing every year with double-digit growth rates.

- Banking Network Reach: Through connections with 2200+ banks and credit unions, Zelle has an estimated coverage of 80% of Americans who have a bank account.

- Business Adoption: Small businesses are adopting Zelle with more than 500 million business transactions amounting to $283 billion in 2024 indicating 32% annual growth.

- Growth Rate: Zelle experienced an average growth rate of approximately 10% a year in the first half of 2025 in the various user groups.

- Market Share: Zelle has a market share of about 54.6% of the value of peer-to-peer mobile payment transactions in the U.S. and is thus the market leader.

Who Owns Zelle?

Zelle is a privately-owned and operated financial services and technology business with its headquarters in Scottsdale, Arizona. Early Warning Services in itself is a common stock owned by seven of the largest banking institutions in America, including but not limited to Bank of America, JPMorgan Chase, Wells Fargo, U.S. Bank, PNC Bank, Capital One, and Truist (formerly BB&T).

This distinctive ownership is a strategic partnering of major banks in which they developed their own payment network to effectively compete with independent fintech platforms such as Venmo, PayPal, and Cash App that were taking large market share in the peer-to-peer payments.

How Does Zelle Work? | Step-by-step Flow

For Sending Money:

- Go to the mobile app of your bank or the Zelle standalone app (standalone app will be shut down in April 2025)

- Go to the Zelle option of your banking menu.

- Choose the option of sending money and then key in the U.S. mobile phone number or email address of the recipient.

- Enter the dollar value that you would like to transfer.

- Include (Non-obligatory) memo/note of payment purpose.

- Check all transaction information carefully (once sent to enrolled users, it is not possible to delete it)

- Check and ship the payment.

- Money is immediately debited from your bank account and forwarded to the recipient.

For Receiving Money:

- Get the alert on the payment coming through text or email.

- In case you are already registered with Zelle, the money instantly gets into your linked bank account in minutes.

- Otherwise, fail to enroll, and follow the link in the notification.

- Choose your bank/ credit union from the list available.

- After registration, follow those enrollment guidelines to confirm your identity.

- Upon enrollment, the amount is deposited directly into your bank account.

- Any further payment is automatic and without any extra effort.

Key Features:

- The transfers get done within minutes to those with accounts (takes up to 3 days for first timers)

- Works 24 hours around the clock, 7 days and 365 days.

- No individual bank account to transact–bank accounts swap money.

- And offered at 2,200+ partner banks and credit unions.

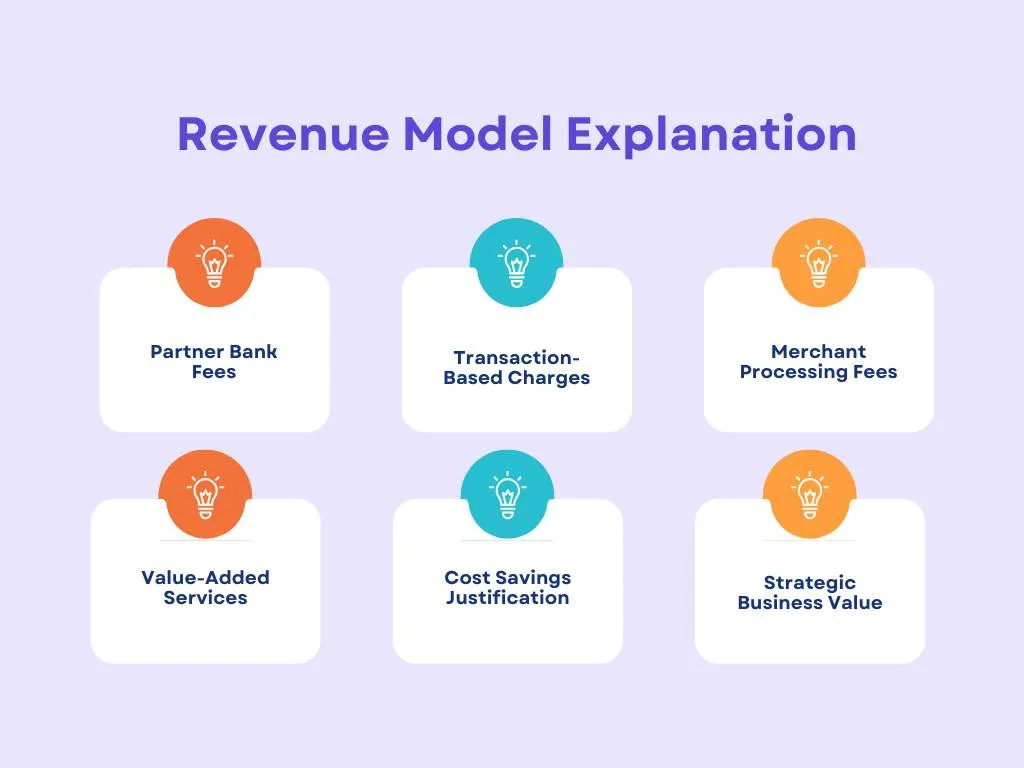

How Does Zelle Make Money Without Charging Users? | Revenue Model Explanation

To answer the question of how Zelle makes money it is necessary to focus on its B2B2C (business-to-business-to-consumer) model. The following are the major source of revenue:

- Partner Bank Fees: Financial institutions have to pay subscription fees to Early Warning Services to have access to Zelle network and technology infrastructure under licence. These charges can be in the form of fixed licensing fees or charged per transaction but the specific form of charge is confidential and differs between institutions.

- Transaction-Based Charges: Banks will pay depending on the number of payments made by using the network of Zelle. The more transactions, the more participating banks pay to remain on the network.

- Merchant Processing Fees: Visa or Mastercard card networks also impose processing fees of about 1% to the merchants when consumers use Zelle to make payments to businesses. Part of this merchant fee is remitted to the card-issuing bank, providing an indirect source of revenue for the Zelle ecosystem.

- Value-Added Services: Zelle generates additional revenue by delivering higher-quality fraud detection, security, reporting analytics, customer behavior analysis, and compliance monitoring to partner banks.

- Cost Savings Justification: Banks voluntarily accept such fees because Zelle will help them retain customers, reduce operational expenses associated with traditional payment services such as paper checks and wire transfers, and avoid customer drift to alternative third-party payment services.

- Strategic Business Value: Zelle does not operate as a stand-alone profit center; instead, it supports the strategic aim of ensuring that payment transactions and customer relationships within the standard banking system are owned by the originating banks.

Who Pays the Cost of Zelle?

The Zelle network has several stakeholders in its ecosystem who have to share the operational costs:

- Participating Banks and Credit Unions: Banks and Credit Unions must shoulder the greatest financial burden by paying fees to licensing, transaction, and technology access fees to Early Warning Services to integrate Zelle into their systems.

- Owner Banks: The 7 large banking institutions that collectively own Early Warning Services make large investments in platform development, infrastructure maintenance, security improvements, fraud mitigation systems, and ongoing innovation.

- Business Merchants: When companies receive payments via Zelle from customers, they are charged processing fees (typically 1 percent) by payment card networks, which helps keep the broader payments ecosystem afloat.

- Indirect Consumer Costs: Zelle does not impose any direct fees on consumers, but users should confirm with their financial institutions whether they have any other bank account fees, including monthly maintenance fees, overdraft fees, or transaction caps on the accounts they use.

- Technology Infrastructure Investment: The costs of implementing robust cybersecurity systems, real-time fraud detection, network reliability, and seamless integrations are borne by the participating financial institutions, based on usage and contractual terms.

- Marketing and Education Costs: Banks, Early Warning Service, and Zelle brand together spend on consumer awareness, fraud prevention, security training, and promotion activity to spur the users and usage of the platform safely.

The core idea is that end users can experience unlimited peer-to-peer transactions, while the banks recognize the strategic value of retaining payments within their systems rather than losing market share to external fintech competitors.

Zelle Net Worth & Market Value (Data Since 2024)

Although Zelle is not publicly traded and does not disclose its exact valuation, the platform’s influence on the market and strategic value are significant. As of 2024, Zelle had handled more than $1 trillion payment volumes, becoming the highest-volume peer-to-peer payment network in the US by transaction volume. The number of its users increased to 151 million, with annual growth doubling.

Zelle is not a classic fintech venture-backed start-up that is seeking an independent valuation. Still, industry observers estimate that the strategic value it can offer to the seven owning banks is enormous. Since competitors such as PayPal are worth tens of billions of dollars on the market, with Venmo generating much of the total income of PayPal, Zelle may be worth a few billion dollars as a utility owned by a bank, yet it is doing the same thing as PayPal, but in a radically different manner than a publicly traded payment organization.

Through mid-2025, Zelle reported ~2 billion transactions worth nearly $600 billion within the first six months — reflecting continued strong growth. While official 2026 figures aren’t yet publicly available, third-party estimates project continued user growth, with around 82 million+ active users in 2026 (note: these are usage estimates, not formal financials).

| Metric | 2024 (Actual) | 2025 (Actual/Partial) | 2026 (Estimated) |

|---|---|---|---|

| Transaction Volume | >$1 trillion/year | ~600 billion in H1 | Likely higher (trend) |

| Transactions Count | ~3.6 billion | ~2 billion in H1 | Continued growth |

| Users (Network) | ~151 M accounts | ~145 M+ (est.) | ~82 M active nodes (usage estimate) |

| Corporate Revenue (EWS) | ~$500 M est. | ~Same (private, no disclosures) | ~Same (assumed) |

| Official Market Value | Not disclosed | Not disclosed | Not disclosed |

Zelle vs Other Payment Apps

| Feature | Zelle | Venmo | Cash App | PayPal |

| User Fees | Completely free | Free for standard transfers; 1.75% for instant; 3% for credit cards | Free for standard; 0.5-1.75% for instant transfers | Free for friends/family via bank; 2.9% + $0.30 for credit cards |

| Transfer Speed | Minutes (instant) | 1-3 business days standard (instant available for fee) | 1-3 business days standard (instant available for fee) | Instant or 1-3 business days depending on method |

| Separate Account Balance | No (direct bank transfer) | Yes (wallet system) | Yes (wallet system) | Yes (wallet system) |

| Debit Card Offered | No | Yes (Venmo Card) | Yes (Cash Card with investing features) | Yes (PayPal Debit Mastercard) |

| Social Feed Feature | No | Yes (public/private transaction feed) | Limited social features | No |

| Bank Integration | Built into 2,200+ bank apps | Requires separate app download | Requires separate app download | Requires separate app download |

| Business Payments | Yes (merchants pay ~1% fee) | Yes (with merchant fees) | Yes (with merchant fees) | Yes (with business fees) |

| Cryptocurrency Trading | No | Yes (limited crypto) | Yes (Bitcoin investing) | Yes (crypto available) |

| Stock Investing | No | No | Yes (stock and Bitcoin) | No |

| International Transfers | No (U.S. only) | No (U.S. only) | Very limited | Yes (extensive international) |

| Daily/Weekly Limits | Up to $5,000/day (varies by bank) | $60,000/week for verified users | $2,500/week for verified users | $60,000/transaction for verified users |

| Fraud Protection | Bank-level security through financial institutions | Limited for authorized payments | Limited for authorized payments | Buyer and seller protection available |

| FDIC Insurance | Yes (through partner banks) | Yes (with Pass-Through Insurance) | Yes (with Cash Card balance) | No for standard balance |

| Payment Reversibility | Not reversible once sent to enrolled users | Limited reversal options | Limited reversal options | Dispute resolution available for goods/services |

| Best Use Case | Fast, free transfers between trusted contacts via existing bank app | Social payments among friends with public sharing | Payments plus investing and financial services | Online shopping and international payments |

Key Distinctions:

- Zelle: Ideal personal transactions This is best when it comes to instant and free bank-to-bank transfers; it is built right into banking apps, and no additional balance management is needed; best for transactions between trusted persons.

- Venmo: Among the younger audiences loved in terms of social payment feed, well accepted by merchants, casual payments among friends and small purchases.

- Cash App: Has more financial services, not just payments, such as stock investing, Bitcoin trading and early direct deposit; targets users who want all-in-one financial platform.

- PayPal: Best for e-commerce and international payments; it offers robust buyer/seller protection and is well-suited to marketplace online shopping.

Conclusion

The explanation of how does Zelle make money shows a business-to-business-to-consumer model that was a disruptive innovation in payment systems. Zelle established a long-term ecosystem where banks keep customers, users get instant free transfers, and it handles more than a trillion dollars a year by providing consumers with absolutely free peer-to-peer transactions and enabling financial institutions to earn revenue by creating a strategic alliance. The key to how Zelle makes money is that it assumes a B2B model of revenue, i.e., it charges banks access to the network, the technology infrastructure, and transaction processing, along with value-added services, instead of collecting fees on individual users.

With its scale of 2,200+ partner institutions, real-time transfers, and integration with leading banking apps, Zelle is redefining peer-to-peer payments. With the future of digital payments still shifting, Zelle’s ownership by large banking institutions, its emphasis on security and speed, and its zero-fee guarantee ensure it will remain relevant in the competitive fintech market.

Explore How Popular Brands or People Make Money:

FAQs

1. Is Zelle absolutely free to users?

Yes, Zelle is free to the consumer to receive and send money. Zelle does not have any transaction fees, monthly fees, or any unknown costs. Nevertheless, you should check with your bank or credit union to confirm whether they impose any account-related fees or transaction limits on your account.

2. Does Zelle earn any money when users do not pay fees?

Zelle earns revenue by imposing fees on banks and credit unions accessing its payment network, technology platform and transaction processing services. Financial institutions pay these fees because Zelle helps them retain customers, compete with fintech platforms, and reduce the costs of traditional payment methods such as checks and wire transfers.

3. Who is the owner of Zelle and why has it been developed?

Early Warning Services, LLC owns Zelle and is owned by seven central U.S. banks, including Bank of America, JPMorgan Chase, Wells Fargo, U.S. Bank, PNC Bank, Capital One, and Truist.

4. Is Zelle applicable to business payments?

Yes, Zelle supports business transactions. When consumers use Zelle to make payments to businesses, the merchants are typically subject to processing fees (generally around 1%) charged by card networks such as Visa or Mastercard, regardless of whether the consumer has paid.

5. Does Zelle outperform Venmo or Cash App?

Zelle is also as secure as a bank because it uses your current banking app and transfers money between two bank accounts without holding funds in a wallet.