Accounting is the basis of sound decision-making and financial transparency in the world of business and finance. Not every accounting is created equally, though. Financial accounting and management accounting are two basic fields that may perplex students and the business owner alike. Although they both are concerned with financial information and are used to make organisations prosper, their purposes and intended audiences are very different.

The difference between financial accounting and management accounting is also important to anyone who wants to figure out the business environment. This paper will deconstruct these two important accounting functions, examine their respective peculiarities, and assist you in comprehending which accounting data is of greatest significance to the various parties in your business career.

What is Financial Accounting?

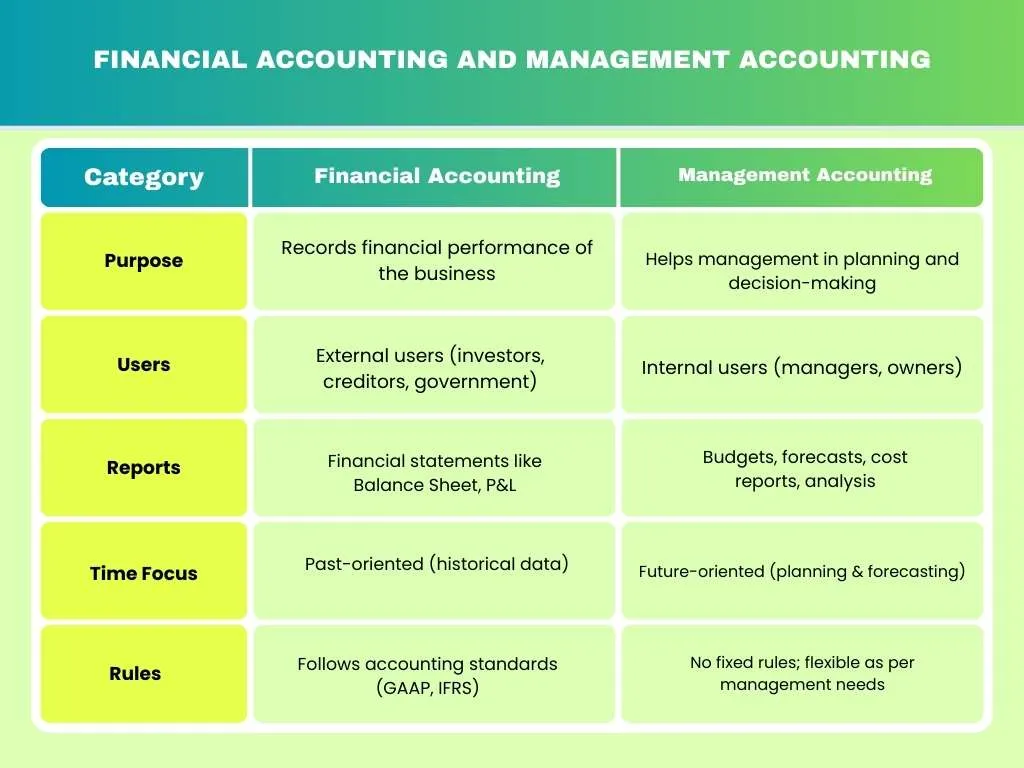

Financial accounting is simply the process of registering, summarising, and reporting the financial transactions of a business to its external stakeholders. It is mainly used to give a true and standardised view of the financial position and performance of a given company within a given period of time. The accounting standards and regulations applied in financial accounting include GAAP (Generally Accepted Accounting Principles) or IFRS (International Financial Reporting Standards) in order to provide consistency, comparability, and reliability.

It is a discipline that makes use of historical information to formulate financial statements such as a balance sheet, income statements, and cash flow statements that mirror what has already transpired in the business, and it is therefore crucial in compliance, taxation, and investor relations.

Key Characteristics

- Adheres to the legal and required accounting standards.

- Concentrates on the past financial records and previous performance.

- Prepares uniform financial reports to be used outside.

- External audit and regulation.

- Prepared reports on a quarterly and annual basis.

Examples

- Shareholder annual financial statements.

- The same was submitted to the government income tax authorities.

- Publicly traded companies’ SEC filings.

- Bank loan applications that a bank mandates a bank to audit financial statements.

- Financial statements are provided to prospective buyers.

Users

- Potential investors and shareholders.

- The tax authorities and regulators of the government.

- Banking and other financial institutions.

- Creditors and suppliers

- Endogenous auditors and rating agencies.

What is Management Accounting?

Managerial accounting or management accounting is the analytical, preparatory and reporting of financial data in a manner tailored to internal decision-making in an organisation. In contrast to its financial counterpart, management accounting is proactive and is aimed at assisting the managers to plan, control and make strategic business decisions. It entails making budgets, projecting performance in the future, cost analysis, project analysis and making elaborate insights that promote efficiency in operations.

Depending on the needs of the organisation, management accounting can be tailored to suit those needs since the external regulations are not obligatory, and the daily reporting may be provided, project-related analysis, or long-term strategic planning tools.

Key Characteristics

- Not controlled by third-party accounting rules.

- Future-oriented and focused on planning.

- Extremely fine and segmental information.

- Reports drawn up as regularly as required (daily, weekly, monthly).

- Has an emphasis on internal decision-making and strategy.

Examples

- Departmental monthly budget reports.

- New product launches-cost benefit analysis.

- Pricing decisions- break-even analysis.

- Comparison of actual and budgeted performance variance.

- Next quarter cash flow projections.

Users

- Top management and the executives of the company.

- Heads of the departments and managers of operations.

- Team leaders and project managers.

- Strategic planning committees.

- Internal business analysts

Key Differences Between Financial Accounting and Management Accounting

| Feature | Financial Accounting | Management Accounting |

| Primary Purpose | External reporting and compliance | Internal decision-making and planning |

| Audience | External stakeholders (investors, creditors, regulators) | Internal management and executives |

| Regulatory Requirements | Mandatory, follows GAAP/IFRS standards | Voluntary, no mandatory standards |

| Time Orientation | Historical (past performance) | Future-oriented (forecasting and planning) |

| Reporting Frequency | Quarterly and annually | As needed (daily, weekly, monthly) |

| Scope | Entire organization as a whole | Specific departments, products, or projects |

| Report Format | Standardized financial statements | Customized reports based on needs |

| Audit Requirement | Often subject to external audit | Not audited externally |

| Level of Detail | Summarized and aggregated | Highly detailed and specific |

| Focus | Accuracy and compliance | Relevance and timeliness |

| Flexibility | Rigid, must follow accounting rules | Flexible, adapts to business needs |

| Cost Consideration | Records historical costs | Uses various cost concepts (opportunity cost, relevant cost) |

Understanding the difference between financial accounting and management accounting through this comparison reveals how each discipline serves a unique and vital role in business operations.

Difference Between Financial Accounting, Management Accounting & Cost Accounting

| Aspect | Financial Accounting | Management Accounting | Cost Accounting |

| Primary Focus | Overall financial position | Decision support | Cost determination |

| Users | External stakeholders | Internal management | Both internal and external |

| Time Frame | Historical | Future-oriented | Both historical and future |

| Regulation | Highly regulated | Not regulated | Partially regulated |

| Reporting | Standardized statements | Customized reports | Cost reports and statements |

| Scope | Entire organization | All business aspects | Cost behavior and control |

| Purpose | Statutory compliance | Strategic planning | Cost optimization |

This further comparison can be employed to explain that, although there is a vast difference between financial accounting and management accounting, cost accounting can be taken as a supplement between the two, which can yield cost information that can be utilized by both the external reporting and the internal management.

Why Understanding Both Types Matters

The difference between financial accounting and management accounting has practical implications to the success of business. Financial accounting keeps you on the right side of the law and it also makes outsiders have confidence in your business. Management accounting assists you in making better choices within the organization. Financial accounting is your investors and regulators report card, management accounting is your road map to get you through the day-to-day business.

Both financial accounting to comply with legal requirements and create credibility and management accounting to identify opportunities, reduce expenses, and strategize growth are employed by smart businesses. The current software has created a new ease of maintaining both systems at the same time, such that the same business transactions are both transformed into a compliance report and a strategic one.

Conclusion

The difference between financial accounting and management accounting is a measure of two different yet complementary ways of interpreting the business performance by using financial data. Financial accounting gives the standardized reliable past record that the external parties require to make sound decisions concerning relationships with the organization. Management accounting offers the insight, the flexibility, and the vision the internal leaders require to make decisions in complex business settings to achieve higher performance. They cannot be ranked as more important than the other because they are used with different purposes to different audiences.

Business students are expected to have the mastery of both fields knowing when each is applicable and the way they complement each other. In the organization leaders must make sure that their enterprises are exemplary in both respects, fulfilling the requirements of the outside world without projecting internal knowledge that leads to competitive advantage. With these comparison and contrasts of these two accounting professions, you are better placed to utilize financial information better in whichever capacity you are acting in the business world.

FAQs

1. What kind of accounting is compulsory to businesses?

Financial accounting is compulsory to the majority of registered businesses since it is necessary to file tax, comply with regulations, and make legal reporting. Management accounting is not mandatory and is applied in accordance with the internal requirements.

2. Are small businesses the beneficiaries of management accounting?

Absolutely! Simple management accounting methods such as budget tracking, cost analysis per product, and cash flow forecasting can help such small businesses make better decisions and increase their profitability.

3. Is it necessary to have different accountants on financial and management accounting?

Not necessarily. Numerous accountants are educated in both disciplines but more extensive organizations might possess specialized units. The small businesses are usually one accountant performing both functions.

4. How frequent are the management accounting reports to be made?

Whenever it is required to make good decisions- this might be daily in case of certain indicators such as cash position, weekly in case of operational reports or monthly in case of overall performance reports.

5. What kind of accounting has more accurate information?

Both are true yet they have varying purposes. Financial accounting focuses on verifiable historical accuracy, whereas management accounting focuses on the relevant information timely which can be estimated and projected to make future planning.